Blog

What You Need to Know About Fund Advertising and FINRA Compliance

Daryn Levesque | 27 May 2026

Shirley Pastrana and Robert Holmes of PINE Advisor Solutions also contributed to this article.

If you work with PINE-distributed products, here's what you need to know about how we manage marketing communications. The short version: before any material goes out the door to investors, advisors, or the public, it needs to be reviewed and approved.

Here's how that breaks down:

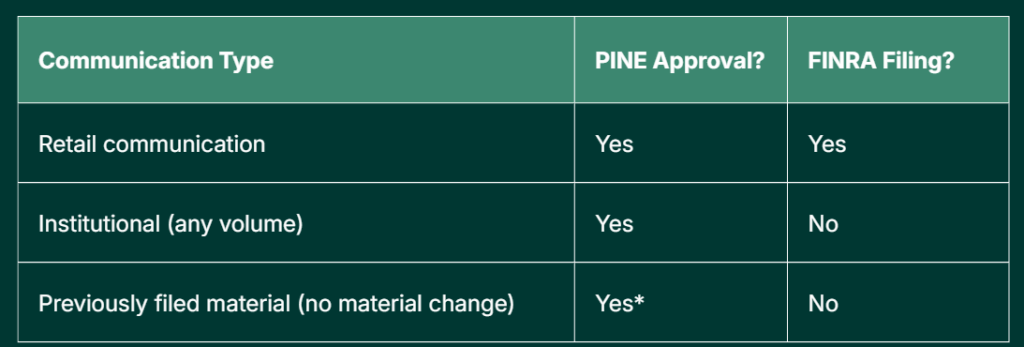

Retail communications covers anything written or electronic that reaches more than 25 retail investors within a 30-day window. For example, websites, fact sheets, fund commentaries, mass emails, print ads, and social media posts. Basically, if it’s made available to the public, it's retail communication.

FINRA rules require a qualified registered principal to approve the material before it's used or filed with FINRA — whichever comes first.

Institutional communications are materials that are used exclusively with institutional investors. For example, government entities, benefit plans with over 100 participants, other FINRA member firms, and most financial intermediaries. Presentations for financial professionals and emails sent only to advisors qualify as an institutional communication.

FINRA rules still mandate pre-approval by a registered principal, but the material isn’t subject to FINRA’s filing requirements. Every piece must carry a prominent label like "For Financial Professional Use Only – Not For Use With The Investing Public," and the institutional audience is not permitted to forward the material to retail investors.

Note: If you're not confident that the institutional-use-only label will be followed, then the material should be treated as a retail communication.

* post-use approval is acceptable

When does FINRA filing apply for retail materials?

Skip the filing?

Institutional communications, article reprints, interactive social media posts, and materials making no investment recommendation are all excluded from FINRA filing — but registered principal approval is generally required.

No matter the audience, FINRA Rule 2210 sets the floor.

When performance numbers appear in marketing material, specific disclosures are required and they must be bolded or italicized:

Standardized performance must include one-, five-, and 10-year average annual returns as of the most recent completed calendar quarter and must account for maximum sales loads and all recurring fees.

Note: Footnote-only disclosures aren’t sufficient in print materials. Performance-related disclosures must appear in the body of the advertisement, next to the referenced data.

Retail and institutional materials are reviewed through PINE’s use of a third-party compliance portal. Best practices include:

Questions? If you're unsure whether something needs review, reach out to PINE's Advertising Review Principal.

If you work with PINE-distributed products, here's what you need to know about how we manage marketing communications. The short version: before any material goes out the door to investors, advisors, or the public, it needs to be reviewed and approved.

Here's how that breaks down:

Retail Communications

Retail communications covers anything written or electronic that reaches more than 25 retail investors within a 30-day window. For example, websites, fact sheets, fund commentaries, mass emails, print ads, and social media posts. Basically, if it’s made available to the public, it's retail communication.

FINRA rules require a qualified registered principal to approve the material before it's used or filed with FINRA — whichever comes first.

Institutional Communications

Institutional communications are materials that are used exclusively with institutional investors. For example, government entities, benefit plans with over 100 participants, other FINRA member firms, and most financial intermediaries. Presentations for financial professionals and emails sent only to advisors qualify as an institutional communication.

FINRA rules still mandate pre-approval by a registered principal, but the material isn’t subject to FINRA’s filing requirements. Every piece must carry a prominent label like "For Financial Professional Use Only – Not For Use With The Investing Public," and the institutional audience is not permitted to forward the material to retail investors.

Note: If you're not confident that the institutional-use-only label will be followed, then the material should be treated as a retail communication.

Pre-Approval and Filing at a Glance

* post-use approval is acceptable

When does FINRA filing apply for retail materials?

- File 10 business days before first use: materials featuring custom performance rankings or security futures.

- File within 10 business days post-first use: anything promoting registered investment companies, direct participation programs, CMOs, or securities derived from a single index, commodity, or currency.

Skip the filing?

Institutional communications, article reprints, interactive social media posts, and materials making no investment recommendation are all excluded from FINRA filing — but registered principal approval is generally required.

The Ground Rules: What Every Communication Must Do

No matter the audience, FINRA Rule 2210 sets the floor.

- Keep it fair and balanced: highlight the risks just as clearly as the benefits.

- No cherry-picking: you can't reference only the profitable past recommendations. Any list must cover at least one full year of recommendations, wins and losses alike.

- Don't predict the future: implying that past performance will repeat is not permitted.

- No misleading omissions: leaving out a material fact is treated the same as saying something false.

- Audience matters: the level of detail should match who's reading it.

- No guarantees: you can't promise an outcome, protect against losses, or guarantee returns.

Performance Data: Handle with Care

When performance numbers appear in marketing material, specific disclosures are required and they must be bolded or italicized:

- Past performance does not guarantee future results.

- Investment return and principal value will fluctuate; shares may be worth more or less than their original cost at redemption.

- Current performance may differ from what is quoted.

- A toll-free number or website for current month-end performance data must be included unless the material already contains month-end data current to within seven business days.

Standardized performance must include one-, five-, and 10-year average annual returns as of the most recent completed calendar quarter and must account for maximum sales loads and all recurring fees.

Note: Footnote-only disclosures aren’t sufficient in print materials. Performance-related disclosures must appear in the body of the advertisement, next to the referenced data.

Submitting Materials and Staying Current

Retail and institutional materials are reviewed through PINE’s use of a third-party compliance portal. Best practices include:

- Submit all materials through the portal before use.

- If PINE or FINRA requests revisions, update and resubmit.

- Performance-heavy materials (e.g., fact sheets, fund reports) should be resubmitted based on their frequency of distribution (e.g., monthly or quarterly).

- All other materials need at least an annual check-in to ensure compliance with any rule updates.

- The fund’s adviser is responsible for keeping prospectuses, holdings information, and performance data current on fund websites.

Questions? If you're unsure whether something needs review, reach out to PINE's Advertising Review Principal.